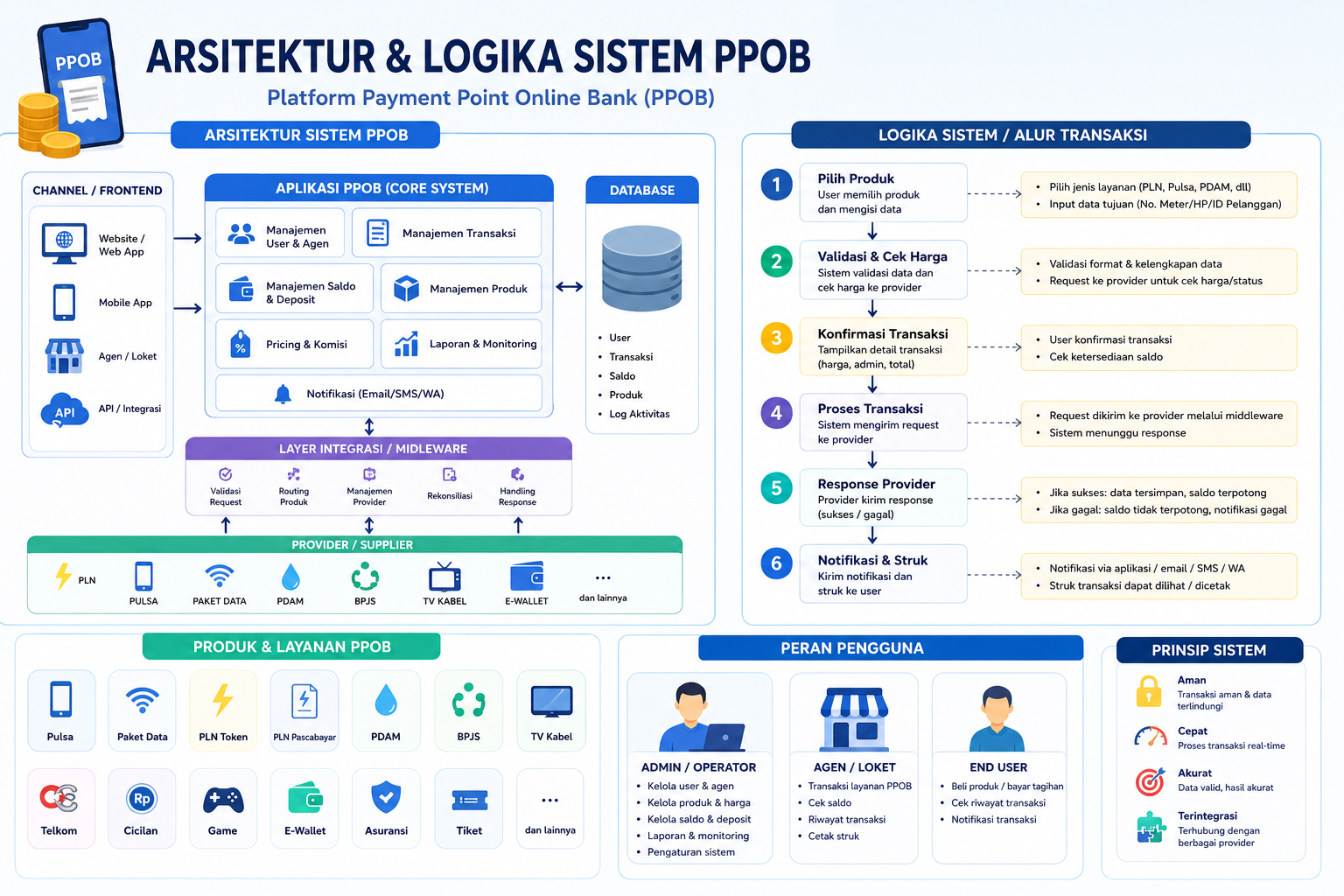

The Architecture & Logic of PPOB Systems in China: A Gateway to Digital Finance Innovation

Introduction: PPOB Systems in China’s Digital Economy

In China, the Payment Point of Service (PPOB) system has evolved into a cornerstone of digital finance, enabling seamless transactions for utilities, subscriptions, and retail services. Unlike traditional payment models, PPOB in China integrates advanced technologies like QR code payments, blockchain, and AI-driven fraud detection, creating a robust ecosystem for both consumers and businesses. This article explores the architecture and logic of PPOB systems through the lens of China’s unique digital finance landscape, highlighting how platforms like WeChat Pay and Alipay have redefined transactional efficiency.

The Layered Architecture of PPOB Systems

The foundation of PPOB systems in China is built on a multi-tiered architecture designed for scalability and security. Here’s a breakdown of its core components:

- User Interface (UI) Layer: This layer interacts directly with users, offering mobile apps, web portals, or physical terminals. In China, QR code-based UIs dominate, allowing users to scan codes for instant payments.

- Payment Gateway: Acts as a bridge between the user and financial institutions. It processes transactions in real-time, leveraging APIs from platforms like WeChat Pay and Alipay.

- Backend Systems: Includes integration with central banks, third-party payment processors, and data analytics tools. In China, these systems often use blockchain for immutable transaction records.

- Security Layer: Employs AI-driven fraud detection, multi-factor authentication, and encryption protocols to safeguard transactions.

Transaction Logic: Real-Time Processing and Fraud Prevention

The logic of PPOB systems in China revolves around speed, accuracy, and security. When a user initiates a payment, the system follows a structured workflow:

- User Authentication: Biometric or PIN-based verification ensures user identity.

- Transaction Authorization: The payment gateway checks the user’s account balance and verifies the merchant’s credentials.

- Fraud Detection: AI algorithms analyze transaction patterns in real-time to flag suspicious activities, as discussed in digital transaction infrastructure studies.

- Settlement: Funds are transferred securely, often utilizing China’s UnionPay network for domestic transactions.

Integration with China’s Tech Ecosystem

China’s PPOB systems are deeply intertwined with its tech giants. For instance, WeChat Pay and Alipay act as intermediaries, connecting users to millions of merchants. These platforms leverage cloud computing for scalability and machine learning to personalize user experiences. The integration of PPOB with China’s digital infrastructure is exemplified by the digital finance revolution, where PPOB serves as a bridge between traditional and modern financial systems.

Challenges and Future Trends

Despite its success, China’s PPOB systems face challenges such as regulatory compliance and cross-border transaction limitations. Future innovations may include:

- Adoption of 5G for faster transaction speeds.

- Expansion of decentralized finance (DeFi) integrations.

- Enhanced AI for predictive analytics in fraud prevention.

Conclusion: PPOB as a Pillar of China’s Digital Economy

The architecture and logic of PPOB systems in China reflect a harmonious blend of technology, user-centric design, and regulatory oversight. By leveraging QR codes, blockchain, and AI, these systems have set a global benchmark for digital finance. As China continues to innovate, PPOB will remain central to its vision of a cashless, interconnected economy.

For further insights into the infrastructure supporting these systems, refer to this detailed analysis on digital transaction ecosystems.