The Architecture and Logic of PPOB Systems: Bridging Traditional and Digital Finance

Introduction to PPOB Systems

Payment Point Online Bank (PPOB) systems represent a critical intersection between traditional financial mechanisms and modern digital transactions. By enabling seamless bill payments and financial services through digital channels, PPOB systems have become instrumental in democratizing access to financial infrastructure. For users in both urban and rural settings, these systems offer a bridge between conventional banking practices and the agility of digital commerce.

Architectural Framework of PPOB Systems

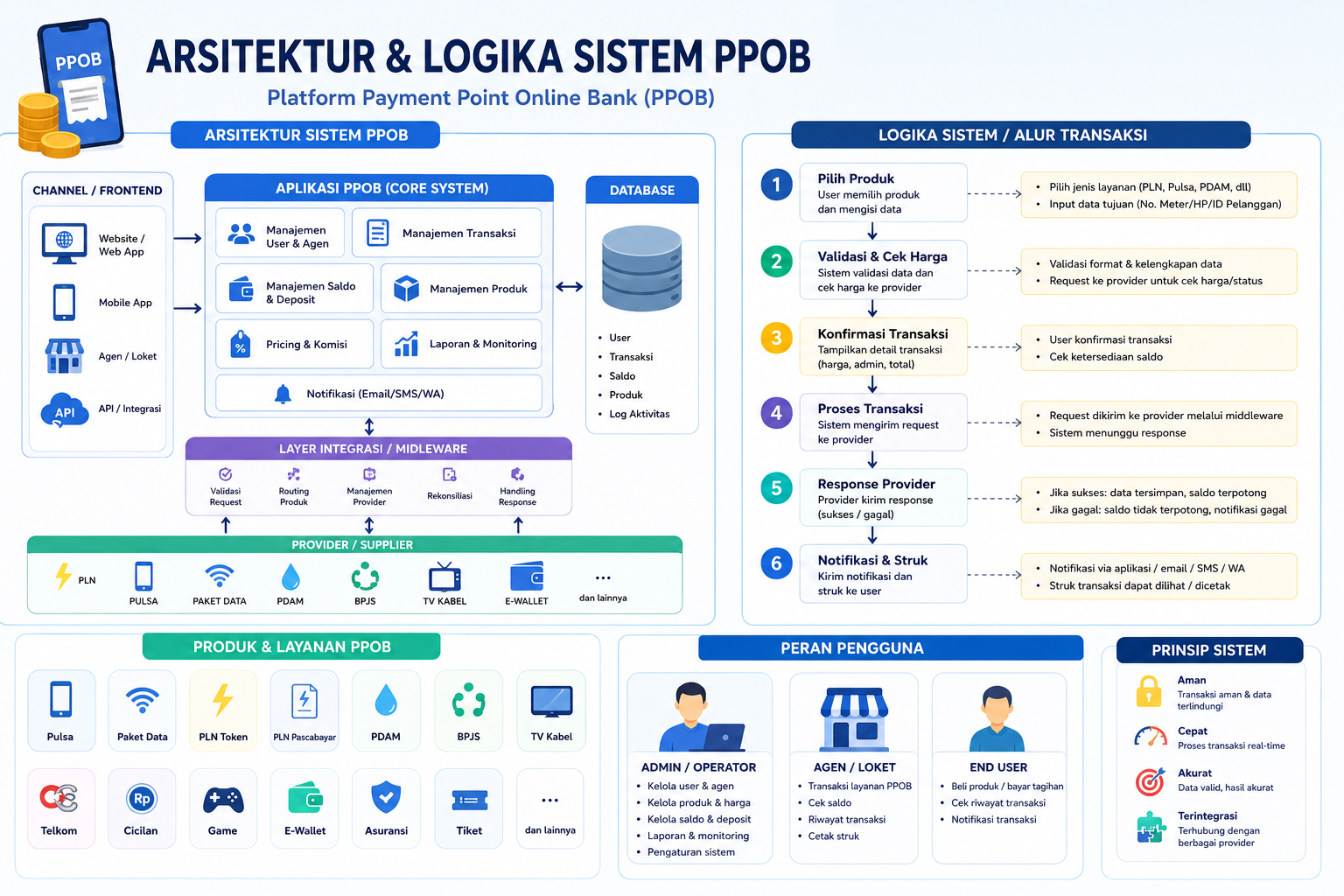

The backbone of a PPOB system is its multi-layered architecture, designed to ensure scalability, security, and user-centric functionality. The core components include:

- User Interface (UI): Acts as the front-end portal for customers, often integrated with mobile apps or web platforms for ease of access.

- Payment Gateway: Facilitates secure transaction processing, connecting users to bank networks and payment processors.

- Backend Infrastructure: Manages data storage, transaction validation, and reconciliation, often leveraging cloud-based solutions for reliability.

- Security Layer: Implements encryption protocols, fraud detection algorithms, and compliance measures to safeguard sensitive financial data.

This architectural design mirrors the principles outlined in previous analyses, emphasizing the balance between technical robustness and user accessibility.

Logical Flow of PPOB Transactions

The operational logic of PPOB systems follows a structured sequence to ensure efficiency and transparency. Here’s a breakdown of the process:

- User Initiation: A user selects a service (e.g., utility bill, mobile top-up) and inputs their payment details via the UI.

- Transaction Validation: The system verifies the user’s credentials and available funds through real-time API calls to banking partners.

- Payment Processing: Funds are transferred securely via the payment gateway, with transaction records updated in the backend database.

- Confirmation & Reconciliation: The user receives a confirmation, and the system reconciles the transaction with financial institutions to maintain accuracy.

This logical flow aligns with the technical frameworks discussed in global digital finance ecosystems, underscoring PPOB’s role in fostering trust and efficiency.

Key Features Balancing Security and Convenience

PPOB systems excel in harmonizing security with user-friendly design. Key features include:

- Multi-Factor Authentication (MFA): Protects against unauthorized access while maintaining a streamlined user experience.

- Real-Time Fraud Detection: Machine learning models analyze transaction patterns to flag suspicious activities instantly.

- API Integration: Allows third-party platforms (e.g., e-wallets) to interact with the PPOB system, expanding service reach without compromising security.

For instance, digital wallets like those depicted in

Scalability and Future-Proofing PPOB Systems

As digital finance evolves, PPOB systems must adapt to emerging technologies and regulatory demands. Key strategies for future scalability include:

- Cloud-Native Architecture: Enhances flexibility and reduces latency, supporting global user bases.

- Blockchain Integration: Explores decentralized transaction models to improve transparency and reduce processing costs.

- AI-Driven Personalization: Tailors financial services (e.g., loan approvals) based on user behavior and credit history.

These innovations position PPOB as a cornerstone of the financial ecosystem, bridging legacy systems with next-generation solutions.

Conclusion

The architecture and logic of PPOB systems exemplify a unique fusion of technological innovation and financial pragmatism. By prioritizing user trust, operational efficiency, and adaptability, these systems are pivotal in shaping the future of global finance. As digital economies expand, PPOB will continue to serve as a vital conduit between traditional banking and the limitless possibilities of digital finance.