PPOB System Architecture & Logic: Decoding the Backbone of Digital Transactions

In the rapidly evolving landscape of digital finance, the Payment Point of Service Business (PPOB) system has emerged as a critical infrastructure for seamless transactions. This article delves into the intricate architecture and logical processes that define PPOB systems, offering a unique perspective on how these frameworks power modern economies.

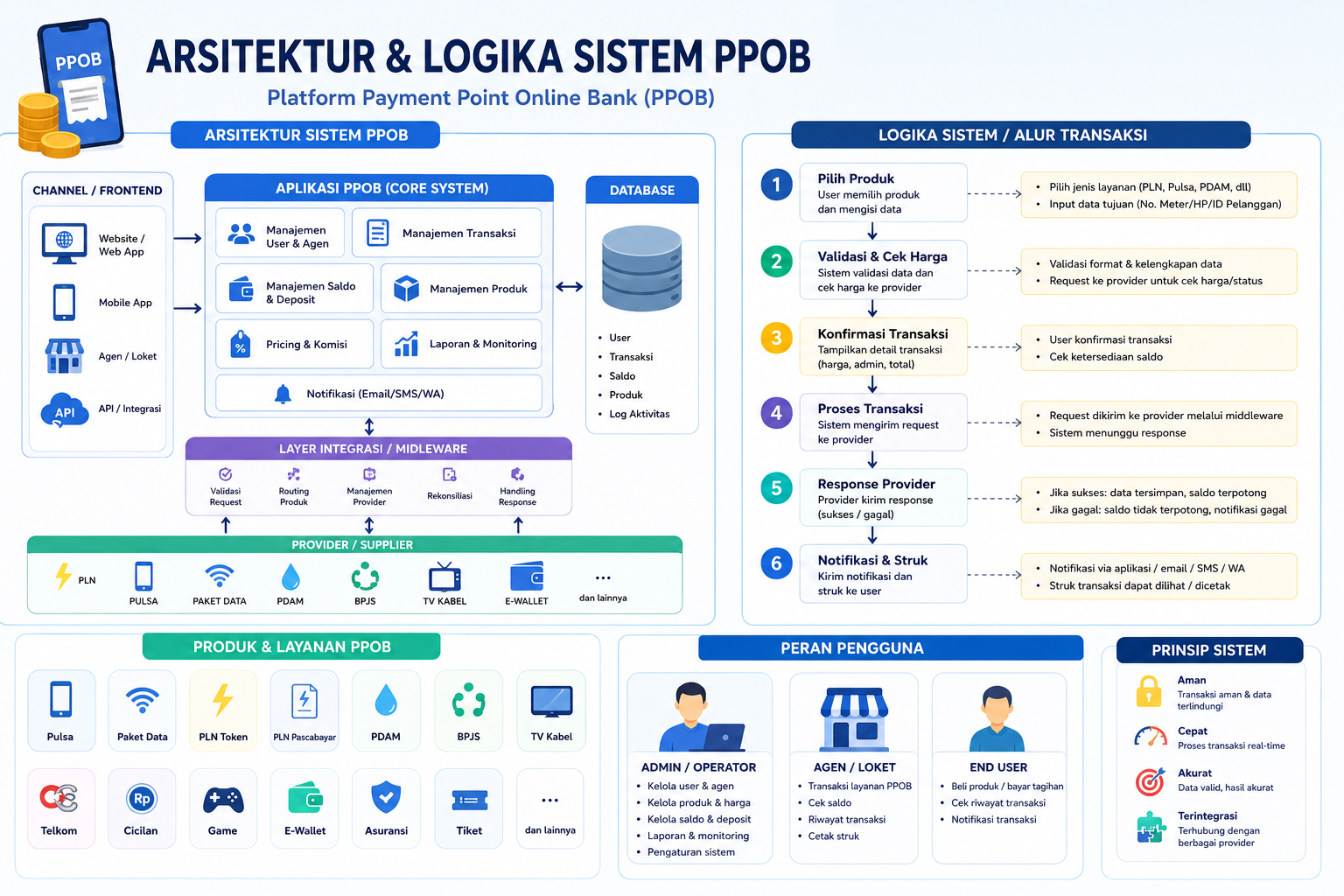

The Core Components of a PPOB System

A PPOB system is typically structured into three primary layers: the frontend interface, middleware processing unit, and backend integration. The frontend serves as the user-facing portal, enabling customers to initiate transactions via mobile apps, web platforms, or physical terminals. The middleware acts as the transaction engine, validating requests, processing payments, and ensuring compliance with regulatory standards. Finally, the backend connects with financial institutions, e-wallets, and other payment gateways to facilitate fund transfers and reconciliation.

Illustration of a PPOB system's layered architecture, highlighting its integration with digital wallets and banking networks.

Transaction Logic: From Initiation to Completion

The transaction lifecycle in a PPOB system follows a precise sequence:

- User Authentication: Biometric verification or two-factor authentication ensures secure access.

- Payment Authorization: The system validates the user's account balance or credit limit in real-time.

- Fund Transfer: Middleware routes the payment through the chosen channel (e.g., WeChat Pay, bank transfer) and confirms receipt with the recipient.

- Post-Transaction Reporting: Data is logged for auditing, fraud detection, and analytics.

This logic is designed to minimize latency while maintaining robust security, a balance critical for high-volume transaction environments.

Integration with Financial Ecosystems

PPOB systems thrive on their ability to interoperate with diverse financial services. For instance, in China's digital economy, PPOB platforms are often linked to innovative digital payment infrastructures, enabling seamless cross-border transactions. Similarly, in Indonesia, PPOB systems integrate with local e-wallets to support microtransactions for utilities and subscriptions.

Scalability and Future-Proof Design

Scalability is a hallmark of effective PPOB architectures. By leveraging cloud-based middleware and modular APIs, these systems can adapt to fluctuating transaction volumes. For example, during peak holiday seasons, PPOB platforms can dynamically allocate resources to handle surges in online shopping payments without compromising performance.

Security Protocols and Compliance

Security is embedded into every layer of the PPOB system. Advanced encryption (e.g., AES-256) safeguards data during transit, while AI-driven fraud detection tools monitor for anomalies in real-time. Compliance with international standards like PCI DSS (Payment Card Industry Data Security Standard) ensures that sensitive financial information remains protected.

Conclusion

The architecture and logic of PPOB systems represent a sophisticated blend of technology and strategic design. As digital economies grow, these frameworks will continue to evolve, integrating emerging technologies like blockchain and AI to enhance efficiency and trust. Understanding their foundational principles is essential for businesses aiming to navigate the future of finance.

For further exploration of PPOB's role in decentralized financial ecosystems, refer to this analysis on AI-driven financial transactions.

Images and references are for illustrative purposes and do not imply endorsement of any service or platform.