PPOB System Architecture & Transaction Logic: Innovating Digital Payments in Modern China

Introduction to PPOB: A Catalyst for China's Digital Economy

The Payment Point Online Bank (PPOB) system has emerged as a cornerstone of China's rapidly evolving digital finance landscape. By enabling seamless, secure transactions between users and service providers, PPOB bridges traditional banking with modern payment demands. This article explores the architectural design and logical framework of PPOB, highlighting its role in fostering innovation and economic growth.

Core Architecture of the PPOB System

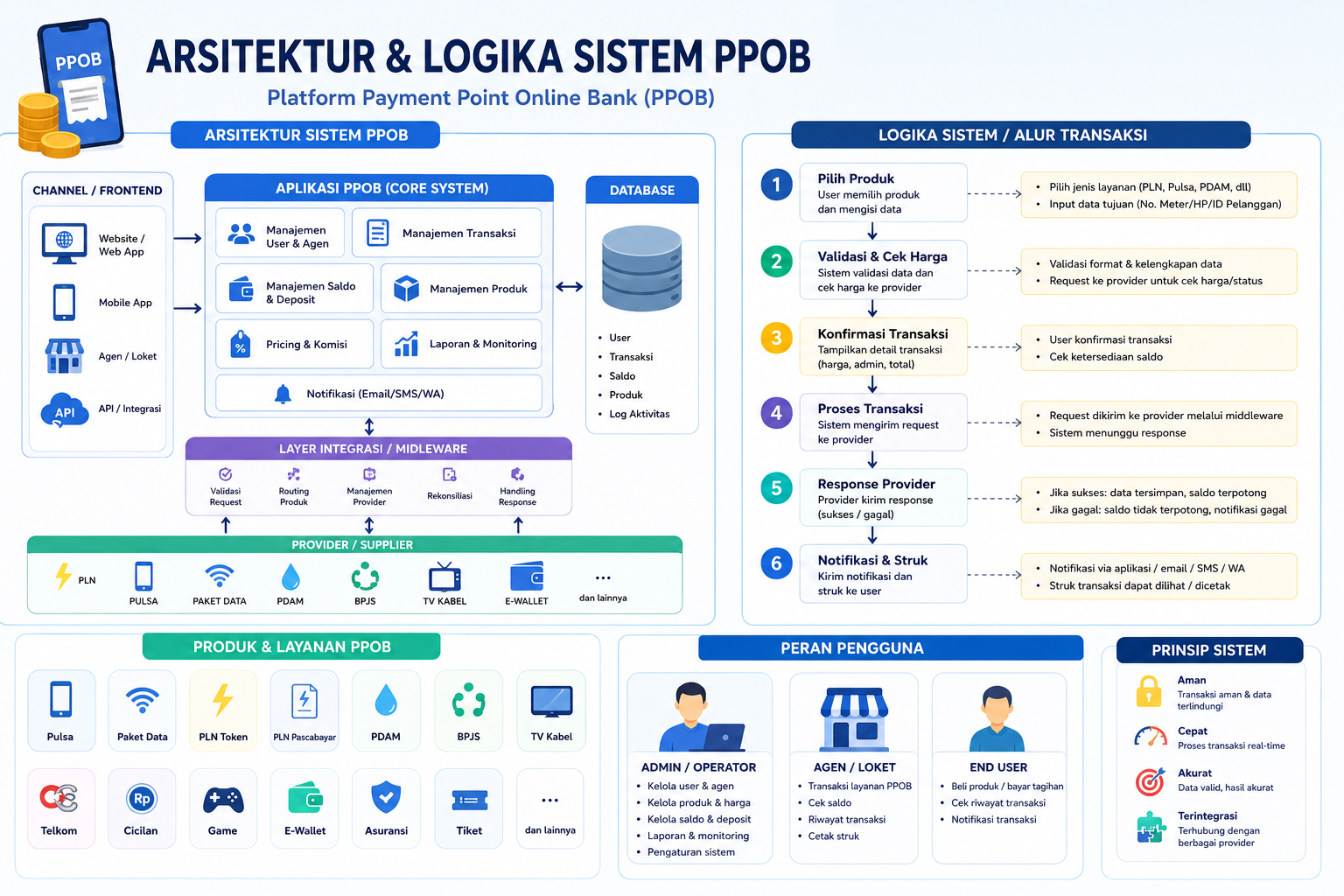

At its core, the PPOB system comprises three primary layers: the user interface, transaction middleware, and backend integration. Each layer plays a critical role in ensuring efficient and secure operations.

- User Interface (UI): The frontend allows users to initiate payments via mobile apps, web portals, or physical terminals. It emphasizes intuitive design and multi-language support to cater to China's diverse population.

- Transaction Middleware: This layer processes real-time data validation, encryption, and routing. It employs AI-driven fraud detection to minimize risks, aligning with China's regulatory standards.

- Backend Integration: The system connects with banks, telecoms, and utility providers through APIs. This interoperability ensures that users can pay for electricity, mobile top-ups, and public services seamlessly.

For deeper insights into how PPOB supports China's digital economy, refer to the article on PPOB's role in financial innovation.

Logical Workflow of PPOB Transactions

The transaction logic of PPOB follows a structured flow to ensure accuracy and security:

- User Authentication: Multi-factor authentication (e.g., QR code scanning, biometrics) verifies the user's identity.

- Service Request Processing: The system identifies the service provider and validates the payment amount using blockchain-based smart contracts to prevent tampering.

- Payment Execution: Funds are transferred through the banking network with real-time confirmation. The transaction is recorded in a distributed ledger for auditability.

- Confirmation & Notification: Users receive alerts via SMS or push notifications, ensuring transparency.

This process mirrors the evolution of systems like PPOB, as detailed in the article "PPOB System Evolution", which highlights its adaptability to emerging technologies.

Security & Scalability: Addressing Modern Challenges

China's digital payment market, valued at over ¥120 trillion annually, demands robust security measures. PPOB employs:

- End-to-end encryption (AES-256) to protect sensitive data.

- Distributed denial-of-service (DDoS) mitigation to prevent service disruptions.

- Dynamic load balancing to handle surges in transaction volume during peak hours.

These features align with China's financial regulations, such as the Regulatory Framework for Payment Services, ensuring compliance and trustworthiness.

Future Trends: Integrating AI and Blockchain

PPOB is poised to adopt advanced technologies like AI for predictive analytics and blockchain for immutable transaction records. For instance, AI algorithms can analyze spending patterns to offer personalized financial advice, while blockchain enhances cross-border payment efficiency.

As China continues to lead in digital finance, the PPOB system exemplifies how architectural innovation and logical precision can drive economic transformation. By prioritizing security, scalability, and user experience, PPOB remains a vital infrastructure for China's digital future.