PPOB System Architecture and Logic: The Invisible Backbone of Modern Digital Transactions

The Silent Architect: Decoding PPOB’s Structural Complexity

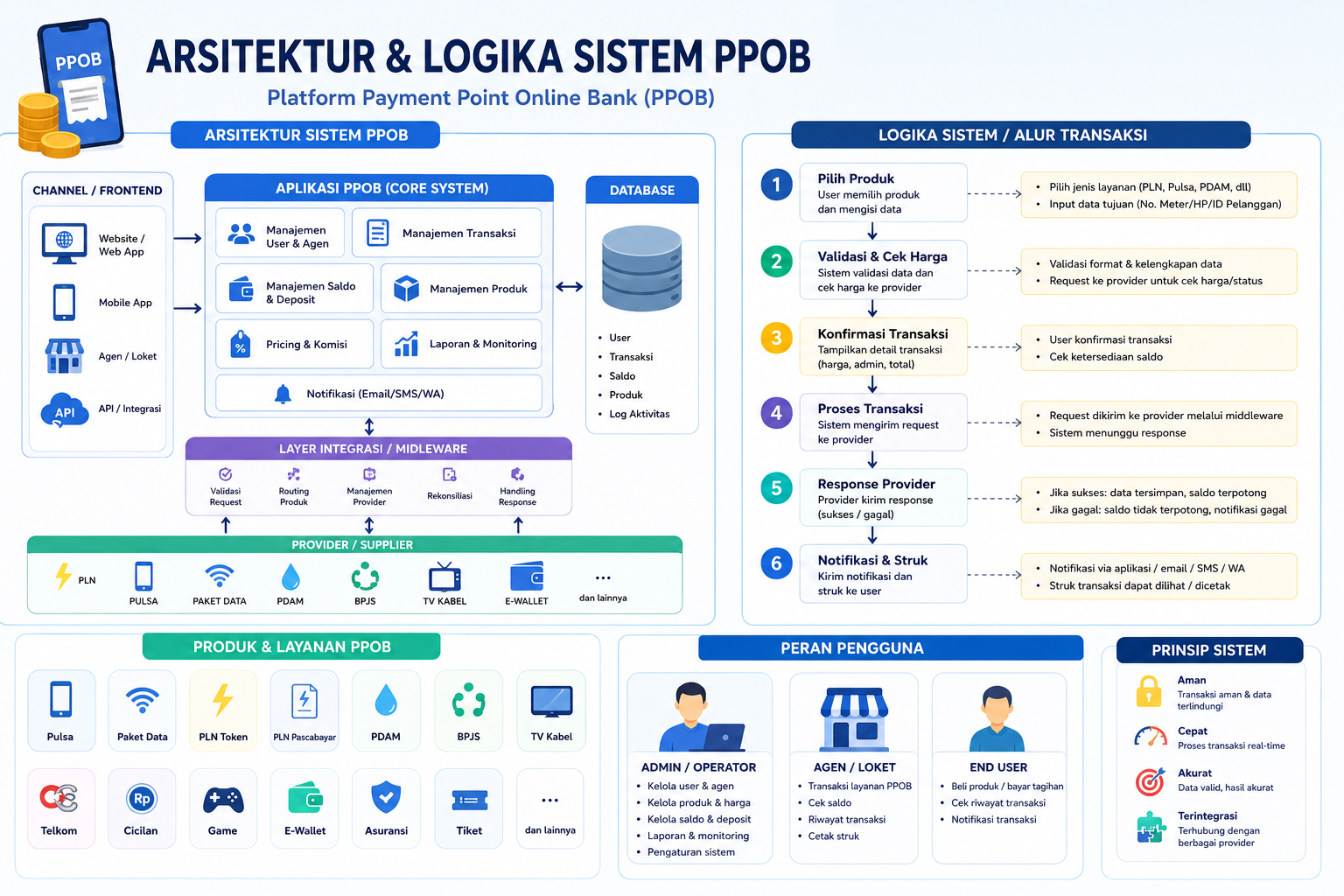

PPOB (Payment Point of Sale Bank) systems are the unsung heroes of modern digital economies, operating like invisible conductors in an orchestra of transactions. Their architecture is a marvel of layered design, blending speed, security, and scalability to handle millions of payments daily. At its core, a PPOB system operates on a multi-layer architecture—a concept explored in-depth in this Japanese article—where each layer serves a distinct purpose.

The foundational layer is the transaction processing engine, responsible for routing payments through secure protocols. Above this lies the business logic layer, which enforces rules for fraud detection and compliance. Finally, the user interface layer interacts with merchants and consumers, ensuring seamless access to payment options like mobile wallets or bank transfers.

Logical Flow: Beyond the Surface of a Button Click

When a user initiates a payment, the system’s logic kicks into motion with a series of micro-operations. First, authentication protocols verify the user’s identity through biometric scans or OTPs (one-time passwords). Next, the system checks account balances and transaction limits against real-time databases. This logic is akin to the Indonesian resource discussing how speed and security are balanced in digital transactions.

- Step 1: User inputs payment request via POS, mobile app, or online portal.

- Step 2: System authenticates user credentials and validates the recipient’s account.

- Step 3: Funds are transferred through encrypted channels, with real-time notifications sent to both parties.

- Step 4: A transaction record is logged in immutable blockchain-like ledgers for auditability.

This logical sequence is not linear but a dynamic web of conditional checks. For instance, if a transaction exceeds a predetermined threshold, additional verification steps (e.g., SMS confirmation) are triggered automatically.

Security: The Unbreakable Fortress of PPOB Logic

Security is embedded into PPOB’s DNA. The system employs end-to-end encryption to protect data in transit and zero-trust architecture to authenticate every request as suspicious until proven safe. This approach mirrors the strategies outlined in this English article, which emphasizes the role of PPOB as a “silent guardian” against fraud.

Key security features include:

- Tokenization: Sensitive data (e.g., credit card numbers) is replaced with unique tokens to minimize breach risks.

- Machine Learning Anomalies: AI models detect unusual patterns, such as sudden spikes in transaction volume.

- Multi-Factor Authentication (MFA): Combines passwords, biometrics, and hardware keys for layered defense.

Scalability and Adaptability: PPOB’s Evolutionary Logic

Unlike rigid legacy systems, PPOB architectures are designed to evolve. They use microservices—independent modules that can be updated without disrupting the entire system. This allows features like cryptocurrency integration or cross-border payment support to be added seamlessly. The Thai article highlights how PPOB systems adapt to regional financial regulations, ensuring compliance without stifling innovation.

For example, in Southeast Asia, where cash usage is still prevalent, PPOB systems integrate QR code payments and agent-based networks. In contrast, European systems prioritize real-time SWIFT transfers and GDPR-compliant data handling.

Future Horizons: Quantum-Resistant Logic and AI-Driven Autonomy

The next frontier for PPOB systems lies in quantum computing and AI. Researchers are already testing quantum-resistant encryption algorithms to future-proof transaction logic against threats posed by quantum decryption. Additionally, AI-driven autonomy could enable systems to self-optimize routing paths during high-traffic periods, reducing latency to near-instantaneous levels.

As global digital economies converge, PPOB systems will likely adopt decentralized identity frameworks, allowing users to control their data while still enabling seamless cross-platform transactions. This evolution will require a delicate balance between innovation and regulatory oversight, ensuring trust remains the cornerstone of digital finance.

Conclusion: The Invisible Symphony of Finance

PPOB systems are more than tools—they are the invisible symphony of modern finance. Their architecture and logic represent a blend of engineering precision and human-centric design, ensuring every transaction, whether paying rent or purchasing groceries, is secure, fast, and reliable. As digital economies grow, so too will the silent guardians like PPOB, adapting to new challenges while preserving the trust that fuels global commerce.