Architecture & Logic of PPOB Systems: Bridging Traditional and Digital Finance in China

Understanding PPOB Systems in China's Financial Landscape

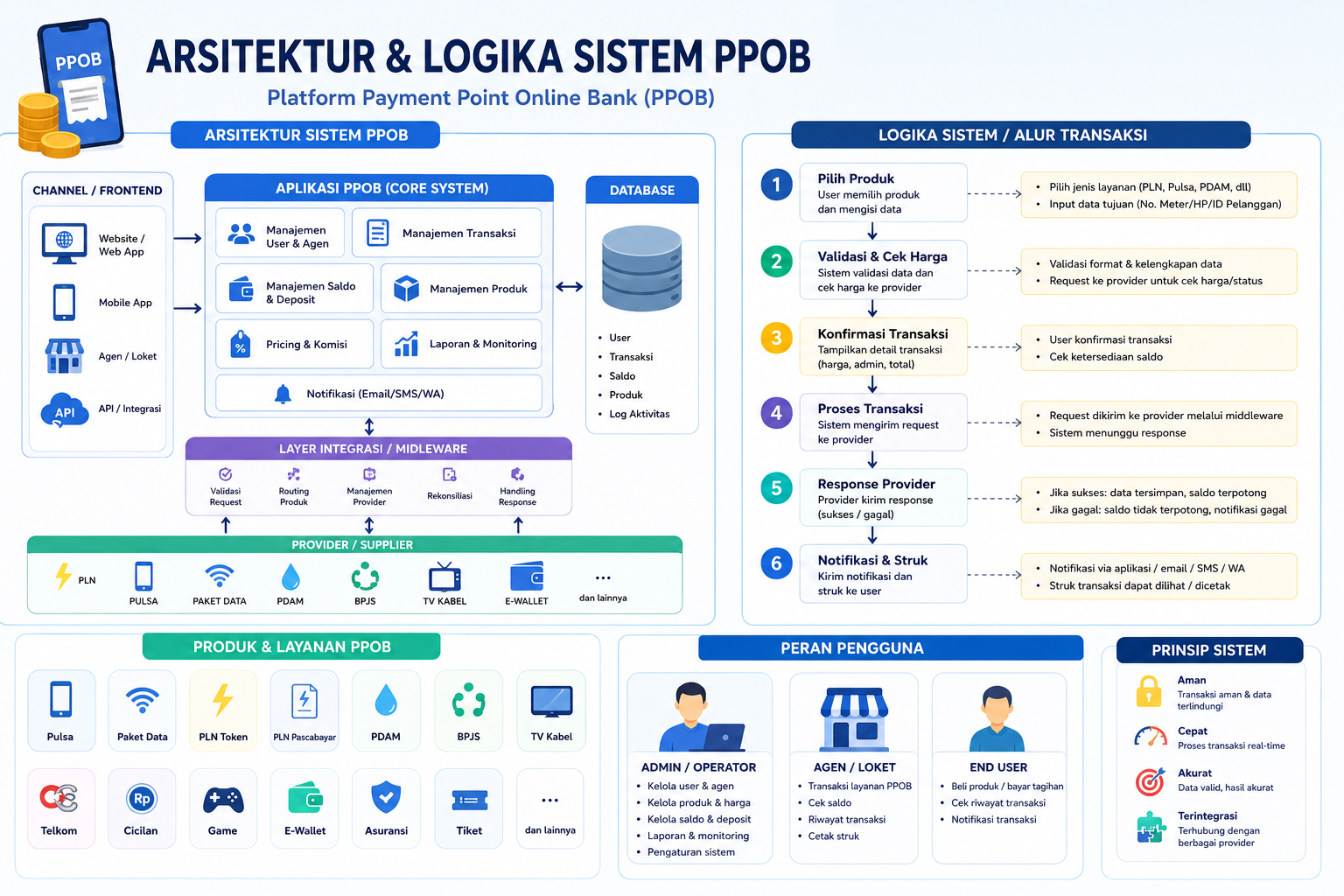

The Payment Point Online Bank (PPOB) system has emerged as a critical infrastructure in China's financial ecosystem, bridging traditional banking with modern digital payment solutions. Unlike conventional payment gateways, PPOB systems operate on a multi-layered architecture that integrates bank networks, third-party service providers, and end-users into a unified transactional framework. This architecture is designed to ensure scalability, security, and compliance with China's stringent financial regulations, such as those enforced by the People's Bank of China (PBoC).

Core Architecture of PPOB Systems

At its core, a PPOB system comprises three primary components: payment gateways, merchant integration modules, and bank reconciliation engines. The payment gateway acts as the front-end interface, enabling users to initiate transactions via mobile apps, websites, or physical terminals. For instance, platforms like WeChat Pay or Alipay leverage PPOB architectures to connect millions of merchants with bank-backed payment channels.

Figure 1: Schematic overview of PPOB system components (Source: PPOB System Architecture in China).

The merchant integration module serves as the middleware, translating transaction requests into standardized formats compatible with banking protocols. This is particularly vital in China, where diverse payment methods—ranging from QR codes to NFC-enabled cards—must coexist within a single ecosystem. The reconciliation engine, meanwhile, ensures real-time settlement between banks and service providers, minimizing delays and fraud risks.

Logical Flow of PPOB Transactions

The operational logic of PPOB systems is rooted in a tokenization mechanism, where sensitive financial data is masked for security. When a user initiates a payment, the system generates a unique token that represents the transaction. This token is then validated across multiple checkpoints, including anti-fraud algorithms and blockchain-based audit trails. For example, China’s cross-bank PPOB initiatives utilize distributed ledger technology to enhance transparency without compromising user privacy.

Integration with Digital Finance in China

China’s digital finance revolution has been accelerated by PPOB systems’ ability to harmonize traditional banking with emerging fintech innovations. By embedding PPOB into mobile wallets and e-commerce platforms, banks like ICBC and CCB have expanded their reach to rural areas where physical branches are scarce. This integration is further supported by regulatory frameworks such as the China Financial Inclusion Development Plan, which mandates interoperability between PPOB and national digital currency projects like the Digital Yuan (e-CNY).

Challenges and Future Trends

- Security Vulnerabilities: While tokenization mitigates risks, PPOB systems remain targets for sophisticated cyberattacks, necessitating AI-driven threat detection.

- Regulatory Compliance: Navigating PBoC’s evolving guidelines on data localization and cross-border transactions poses operational challenges for multinational PPOB providers.

- Scalability: As transaction volumes surge, PPOB architectures must adopt cloud-native technologies to handle peak loads without latency.

Looking ahead, the fusion of PPOB systems with AI and IoT promises to redefine financial services in China. For instance, AI-powered chatbots integrated with PPOB could automate dispute resolution, while IoT-enabled devices might facilitate real-time microtransactions for smart city applications. These advancements align with China’s vision of a cashless society, where PPOB systems serve as the backbone of seamless, secure, and inclusive financial infrastructure.

Conclusion

The architecture and logic of PPOB systems in China reflect a strategic balance between innovation and regulation. By dissecting their multi-tiered design and tokenized transaction models, stakeholders can better appreciate how these systems empower both urban and rural economies. As China continues to lead global fintech adoption, the evolution of PPOB will remain a focal point for integrating legacy banking systems with the digital future.

To explore deeper insights into PPOB’s role in digital finance, refer to our analysis on building an inclusive financial ecosystem or the technical breakdown of bridging traditional and digital finance.