The Architecture and Logic of PPOB Systems: A Strategic Blueprint for Digital Transaction Ecosystems

Introduction to PPOB Systems: Bridging the Gap Between Traditional and Digital Finance

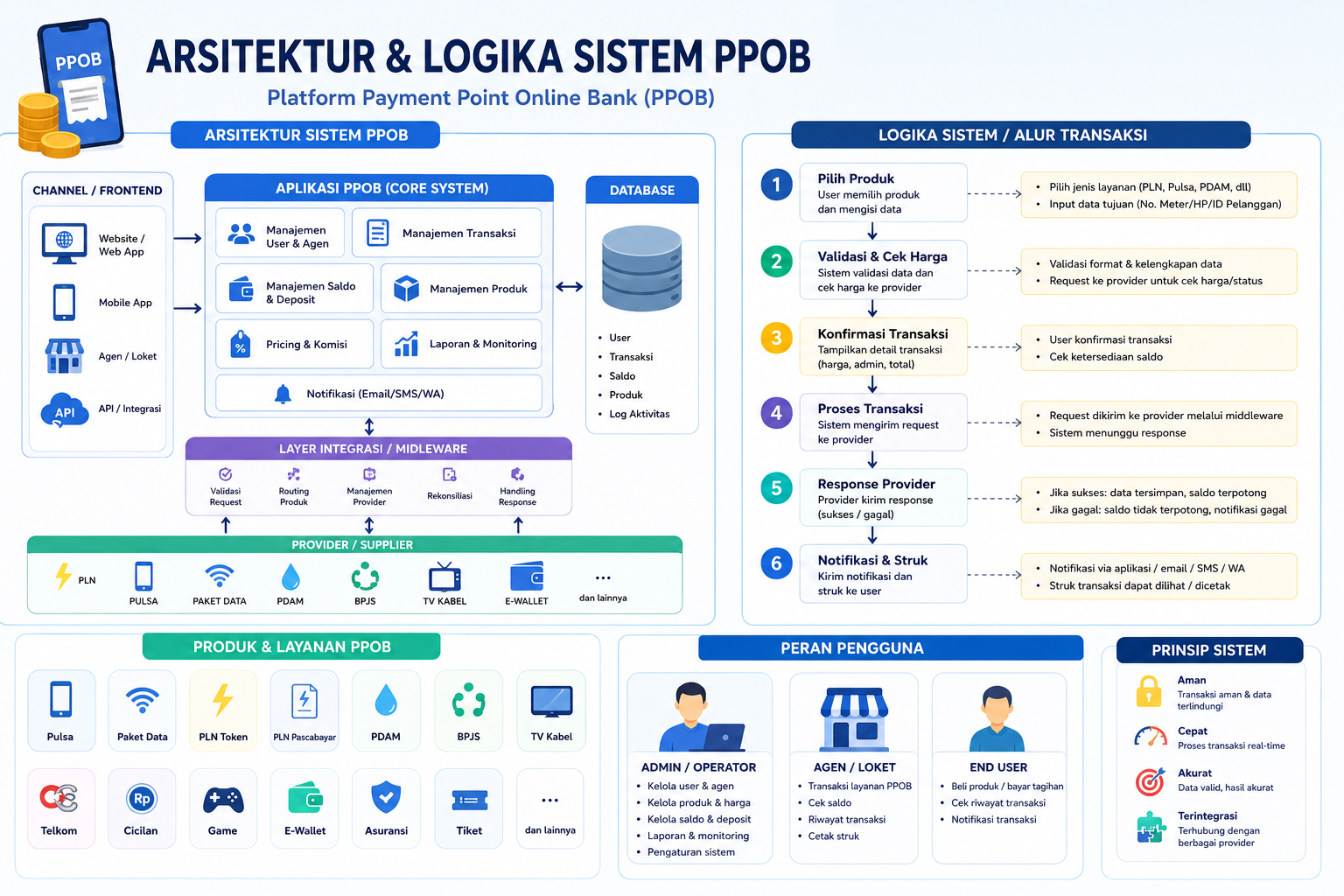

The Payment Point Online Banking (PPOB) system has emerged as a critical infrastructure in modern digital economies, particularly in regions like China where mobile payments and e-commerce dominate. At its core, PPOB acts as a bridge between traditional banking systems and digital transaction platforms, enabling seamless, secure, and real-time payments. This system is not merely a technological tool but a complex network of architecture and logic designed to adapt to the dynamic needs of businesses and consumers alike.

To understand its significance, we must dissect its architecture and operational logic. The system comprises layers—including user interfaces, payment gateways, backend processing engines, and integration APIs—that work in harmony to ensure reliability, scalability, and security. For instance, the PPOB system's neural network-like design allows it to process millions of transactions per second while maintaining data integrity. This is akin to the human nervous system, where signals are transmitted efficiently across interconnected nodes.

Decoding PPOB Architecture: A Layered Approach

The architecture of a PPOB system is typically divided into four core components:

- User Interface (UI): This is the front-end layer where customers interact with the system, such as mobile apps or web portals. In China, this often integrates with popular platforms like WeChat Pay or Alipay.

- Payment Gateway: Acts as the middleware that encrypts transaction data and communicates with banks or third-party processors. It ensures secure data transmission using protocols like TLS/SSL.

- Backend Processing Engine: Handles transaction validation, fraud detection, and settlement. This layer is critical for maintaining compliance with financial regulations and minimizing latency.

- Integration APIs: Enable the system to connect with external services, such as banking institutions, logistics providers, or CRM tools, creating an ecosystem of interconnected services.

Each layer operates independently but is designed to synchronize seamlessly. For example, when a user initiates a payment via their mobile app, the request flows through the UI to the payment gateway, which then authenticates the transaction with the bank. This layered approach not only enhances scalability but also allows for modular updates without disrupting the entire system.

The Logic Behind PPOB: Transaction Flow and Decision-Making

The logic governing PPOB systems is rooted in a combination of real-time decision-making and rule-based processing. When a transaction is initiated, the system evaluates several parameters:

- Account balance verification

- Risk assessment (e.g., fraud detection algorithms)

- Compliance checks (anti-money laundering protocols)

- Routing instructions (e.g., directing payments to the correct recipient)

This logic is often implemented through a state machine model, where each transaction progresses through predefined states (e.g., "Pending," "Approved," "Failed"). For instance, if a transaction is flagged as high-risk, the system may pause it and request additional verification, such as SMS or biometric authentication. This ensures that the system remains both efficient and secure.

Moreover, the integration of machine learning algorithms allows